As more big tech companies want to grow and take over the financial tech space, Apple already offers few financial services like Apple Wallet, Apple Pay and Apple Card. However, it’s reasonable to believe that Apple is interested in taking a step further, become a relevant player in the financial sector and potentially be your next bank. Here are 5 reasons why Apple could do so:

1. Apple enjoys a strong reputation and a loyal client base.

Apple has become a new body part, a lifestyle brand. Adding more financial services to the iPhone is another way for Apple to become an even more integral part of its customers’ lives, creating a higher barrier for them to switch hardware providers. Consumers put their faith in Apple due to what the company stands for and its reputation. They know Apple has a solid foundation to stand upon and will be there for them in the years ahead.

They also know they have the money to invest in research and development. As a result, the services will only continue to get better and better.

Apple customer base is not only loyal but also vast and international. According to Apple, there are currently 1 billion active iPhones globally, and in the United States alone, 45.3% of smartphone users have an iPhone. Thus, if customers can trust Apple with their bank accounts, that could be “the winning punch” against other credit cards with similar perks. Lastly, Apple has the full support of millennials, a generation that looks at banking differently due to the technology they grew up with.

2. Apple knows how to provide a good customers experience.

2. Apple knows how to provide a good customers experience.

A common complaint with traditional banking systems is that they lack a user-friendly interface to view transactions and make operations, from everyday banking transfers to trading securities. Apple is very good at making complex processes appear simple to the end-user. As a result, customers would be able to engage with their banking platform in a clean and straightforward interface that provides them with a snapshot of their financial situation. By acquiring or partnering with powerful personal financial management fintechs,

Apple would provide customers with clear insight and possible actions that they could take to get the most from banking provision. Moreover, Apple could leverage its relationship with the retailers and manufacturers to provide a set of rewards to customers, like cash-backs and incentives. Summing up, at Apple they know what consumers want and how to deliver.

3. Apple needs to find new ways to sell iPhones.

Over time big tech companies need to keep innovating. However, there is a limit on how much Apple can increase profits when it comes to new iPhone designs or by adding new subscription services. The financial industry would be a way to keep growing and turn into a mega big tech company. However, the attractiveness of the banking sector for Apple is not only in its financial return.

Apple’s interest is primarily in becoming an even more integral part of its customers’ life, creating higher barriers for them to switch hardware providers. Moreover, if Apple will be able to provide a superior banking experience, non-iPhone holders may be incentivized to purchase an iPhone to access these services

4. Apple is sitting on a massive pile of unused cash.

Apple has currently around $200 billion in cash on hand. That’s more than the market capitalization of Goldman Sachs itself. Such a significant amount of cash it’s vital to finance acquisitions of fintechs or develop the necessary extensive banking expertise. Moreover, assuming Apple is interested in becoming a full-stack bank, having cash available is essential to satisfy the regulatory issues it will have to deal with to become a banking system.

5. Data Analytics expertise and security.

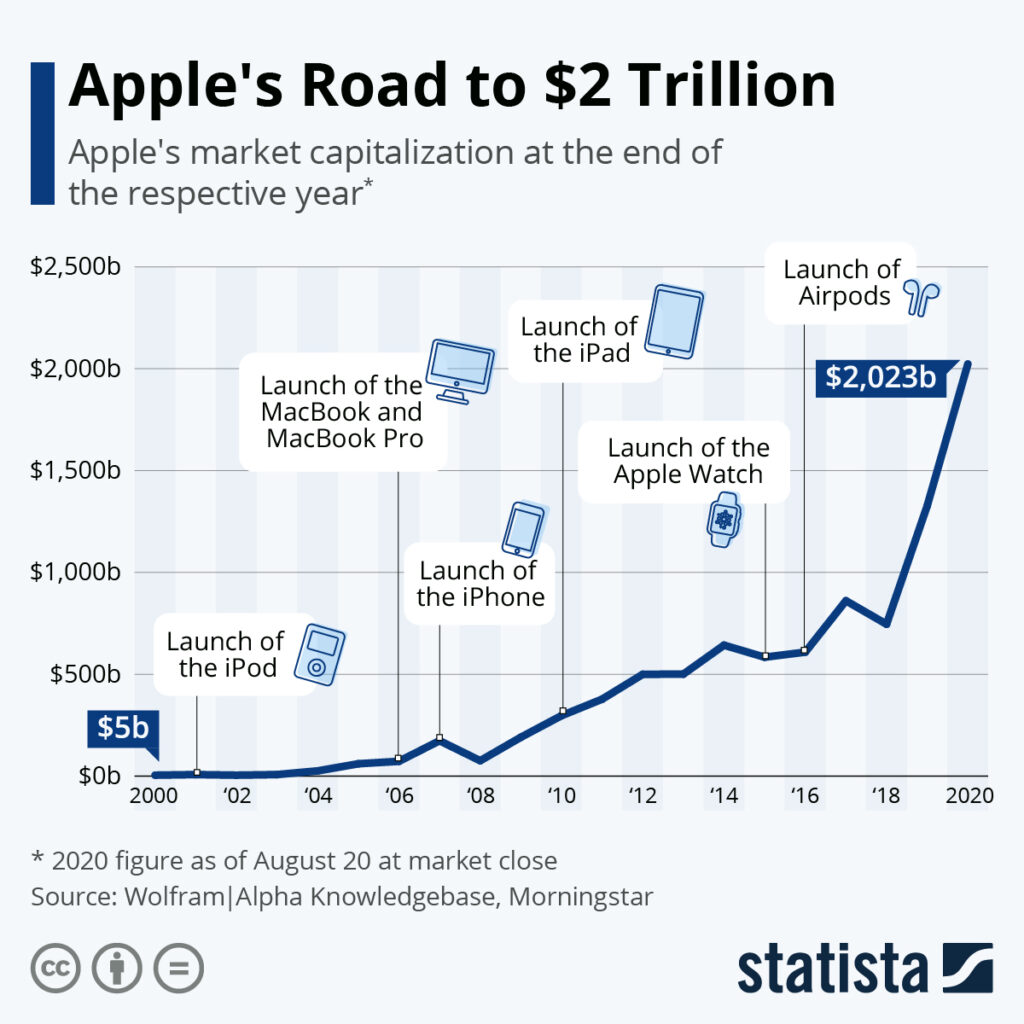

source: Statistica

Apple is a market leader in managing and handling data. Ryan Gilbert, general partner at Propel Ventures, says “money is just a form of data, and Apple has been great at managing access to data. They’ll take the same approach to money”. Moreover, Apple is known for being able to provide customers with heightened security, a crucial aspects when it comes to payments and banking. All the new devices embed biometric security, either “Touch ID” or “Face ID”, which are currently used to authorize payments through Apple Pay and Apple Card.

So, will Apple ever become a bank?

As stated by Sarah Kocianski, Head of Research at fintech consultancy 11:FS, “Apple, like others big tech firms, will continue to add services that are peripheral to banking to their existing offerings, without going full-stack banking. The headache of getting and maintaining a banking license would likely be considered too big a risk for these companies. Instead, they will continue to operate with licensed partners”. This appears to be the most probable path, at least in the next years. However, not being a full-stack bank won’t prevent Apple from disrupting the banking industry.

This article was published by banq. The original article can be found here.