Neobanks Face Setbacks Amid High Cash Burns and Little Revenue Streams

by Fintechnews Switzerland August 15, 2022A challenging economic environment, diminished funding and valuations, and increased scrutiny of regulators have put tremendous stress on neobanks around the world. Over the past few years, the industry has seen its fair share of business failures often due to high cash burns with little or no revenue streams, a new analysis by WhiteSight, a research firm focused on the fintech space, shows.

The analysis, published earlier this month, looks at past failures and setbacks in the digital banking and neobanking sector, delving into business closures, country exits, license application withdrawals and business pivots to understand the areas in which digital challengers are struggling.

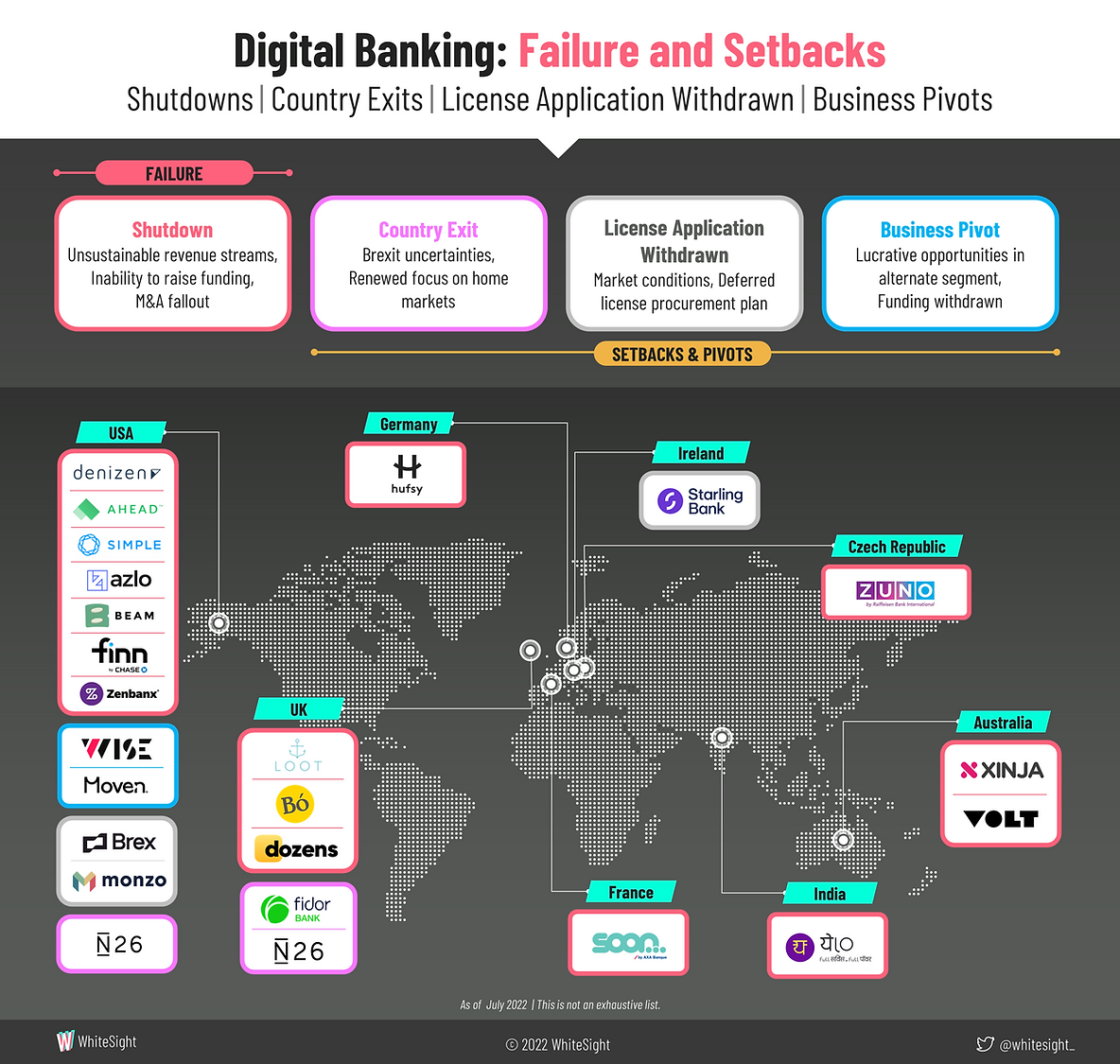

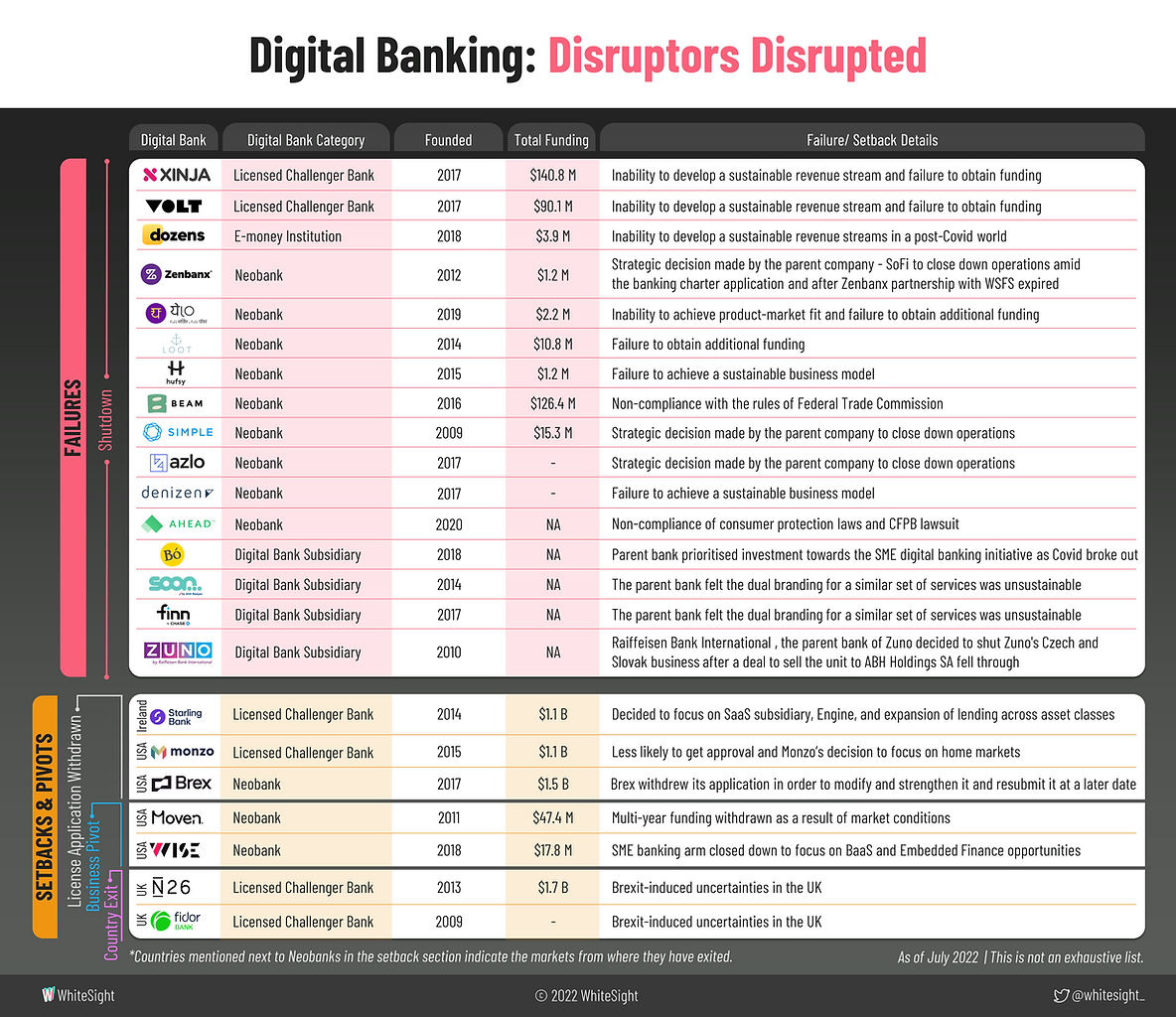

According to the report, at least 16 neobanks and digital banks have closed down around the world over the past couple of years, most often due to their inability to develop a sustainable revenue spurt and secure funding.

In particular, the research found that the US saw a majority of independent neobanks struggling to survive.

Denizen, a San Francisco-based challenger bank incubated out of BBVA’s New Digital Business Unit, shut down in 2019 after just one year of operation. According to WhiteSight, the neobank, which provided a global, borderless account for expat banking, faced difficulties in achieving the scale required to sustain operations.

For Beam Financials, an American mobile savings app, the business’ closure was forced by regulators. In 2021, the company ceased operations under a tentative settlement with the Federal Trade Commission (FTC) after a 2020 CNBC investigation revealed that dozens of customers were unable to get their money out.

The company was mandated to refund approximately US$2.6 million in customer deposits and interest, and banned from operating a mobile banking app or any other product or service that could be used to deposit, store, or withdraw funds. It also was prohibited from misrepresenting the interest rates, restrictions, and other aspects of any financial product or service.

Beyond the US, other regions including Asia-Pacific (APAC) and Europe, have also recorded notable business failures.

In India, Yelo Bank ceased operations in 2021 after failing to find product-market fit and raise follow-on funding. Prior to its closure, Yelo Bank, which focused on gig workers, had raised over US$80 million and had garnered more than 4 million downloads on its app.

In Australia, at least two licensed challenger banks had to shut down after unsuccessful fundraising efforts and failing to develop sustainable revenue streams.

Digital bank Xinja, which managed to amass more than 37,000 customers, collapsed when it started paying customers interest on their deposits before earning income from lending.

In late 2020, the company announced that it would discontinue its transaction and savings account products, and return its authorized deposit-banking institution license, citing “COVID-19 and an increasingly difficult capital-raising environment affecting who is willing to invest in a new bank” as the main reasons why it is pivoting away from being a bank.

Rival Volt Bank has suffered the same fate, announcing in June 2022 that it would shut down, returning deposits and selling its mortgage book after failing to raise sufficient funds to support the business.

Volt Bank was the first startup to gain a banking license back in 2019, and had raised a total of A$212 million before closing down.

In the UK, neobanking apps Loot and Dozens went out of business in 2019 and 2022, respectively, after running out of cash. Loot, which offered a digital-only current account aimed at students and millennials, had around 250,000 registered accounts, and Dozens, a banking app offering a slew of budgeting and analytics tools to help users to save and invest more efficiently, claimed some 60,000 customers.

Neobanks failures and setbacks by country, Source: WhiteSights, 2022

Besides business closures, the WhiteSight research also looks at notable challenges and stumbles faced by neobanks, noting that a number of players have put an halt on their expansion plan, focusing instead of trimming unnecessary spending and profitability.

German licensed digital bank N26 closed its UK operations in 2020 citing difficulties created by Brexit, and in 2022, it pulled out of the US after acknowledging that the investment and management time required in the country was leaving N26 too stretched.

N26 served about 200,000 customers in the UK and 500,000 in the US.

In the US, Solid, formerly known as Wise, pivoted in 2020 from small and medium-sized enterprise (SME)-focused neobanking to embedded business banking. Today, the company provides a digital banking stack built for platforms and banks, focusing on opportunities in the embedded finance and banking-as-a-service (BaaS) spaces.

Neobanks failures and setbacks by category, Source: WhiteSights, 2022

Despite being one of the most talked-about fintech segments of the past decade, neobanks have struggled with profitability. Consulting firm Simon-Kucher estimates that only a mere 5% of the world’s reported 400 digital banks are actually reaching breakeven, with most earning less than US$30 in revenue per customer per year. Moreover, cash burn rates are stellar for several banks, with annual losses exceeding US$100 million in some cases.

Featured image credit: Edited from freepik