Though blockchain-based security tokens hold many potentials, they also have their own limitations and must evolve to address several key challenges, according to a new paper by academics at the Rotterdam School of Management.

In a paper titled Security Token Offerings, the scholars from Erasmus University of Rotterdam (Daniel Liebau, Thomas Lambert and Peter Roosenboom) look at the nascent security token market and delve into the numerous challenges current offerings present, arguing that security tokens must now morph into so-called native digital securities to reach their full potential.

Native digital securities: the next generation of securities

According to the paper, security tokens have three major limitations. Firstly, they are only a digital presentation of an investment and not the product itself, implying that legally, the primary record in many jurisdictions is still paper-based or stored in a government-owned centralized database.

Secondly, since most security tokens are developed on the ERC-20 protocol, the full lifecycle of a security cannot be depicted off the shelf, and the comprehensive financial-product term sheets cannot be represented.

Finally, forks represent an important technical challenge, posing important cybersecurity risks.

In light of these limitations, the paper claims that the next generation of securities won’t just be digital representations of existing paper securities, like security tokens, but instead, will be programmable securities that are digital natives on the blockchain.

The paper refers these as native digital securities and defines them as “a legally accepted primary record of securities, created as smart contract on a distributed ledger.”

With native digital securities, on-chain amendments can be easily and cheaply executed and viewed by stakeholders, increasing thus transparency. Native digital securities can also come with a description language depicting all possible features and variants of an investment product. This description language would enable both digital creation of investment products with any combination of corporate actions and securities product features that could all be executed cheaply on-chain.

Additional potential benefits of programmable securities include the potential for barter-trade equity of one company against another, the ability to display features that reduce legal disputes, as well as the possibility to develop smart contract-based stock-option plans for employees that automatically exercise when agreed objectives are achieved.

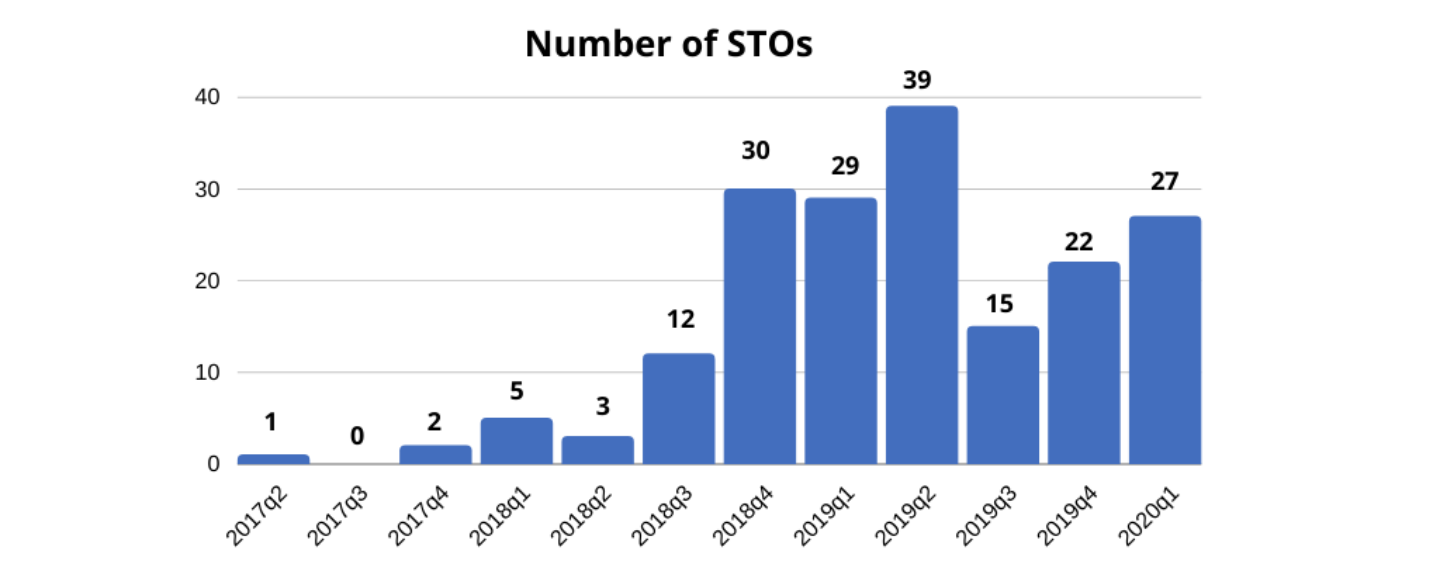

The security token market

The security token market truly emerged after the end of the initial coin offering (ICO) market bubble in the second half of 2018. Though still nascent, the industry is growing steadily, and although dispersed geographically, security token offering (STO) activity is concentrated in jurisdictions with accommodating securities laws.

The study, which analyzed more than a hundred STOs, found that the USA was the preferred location to issue a security token, followed by the Cayman Islands, the UK, Switzerland and Singapore.

In the future, jurisdictions that enact new laws to govern STOs such as Liechtenstein are expected to become fertile ground for native digital securities, the report says.

Liechtenstein’s Blockchain Act, which came into force in January 2020, aims to be a “comprehensive regulation of the token economy.” It contains provisions on registration and disclosure requirements for those that generate or issue tokens.

Trading volume of security tokens almost reached US$22 million in August 2020, a 163.24% increase compared to July 2020, according to Security Token Group’s monthly market report. Market capitalization surpassed US$486 million in August 2020, up 18.15% from July 2020.

tZERO was the biggest security token by market capitalization (US$427 million), followed by Overstock Digital Voting Series A-1 Preferred Stock (US$272 million) and tZERO Preferred Equity (US$131 million).