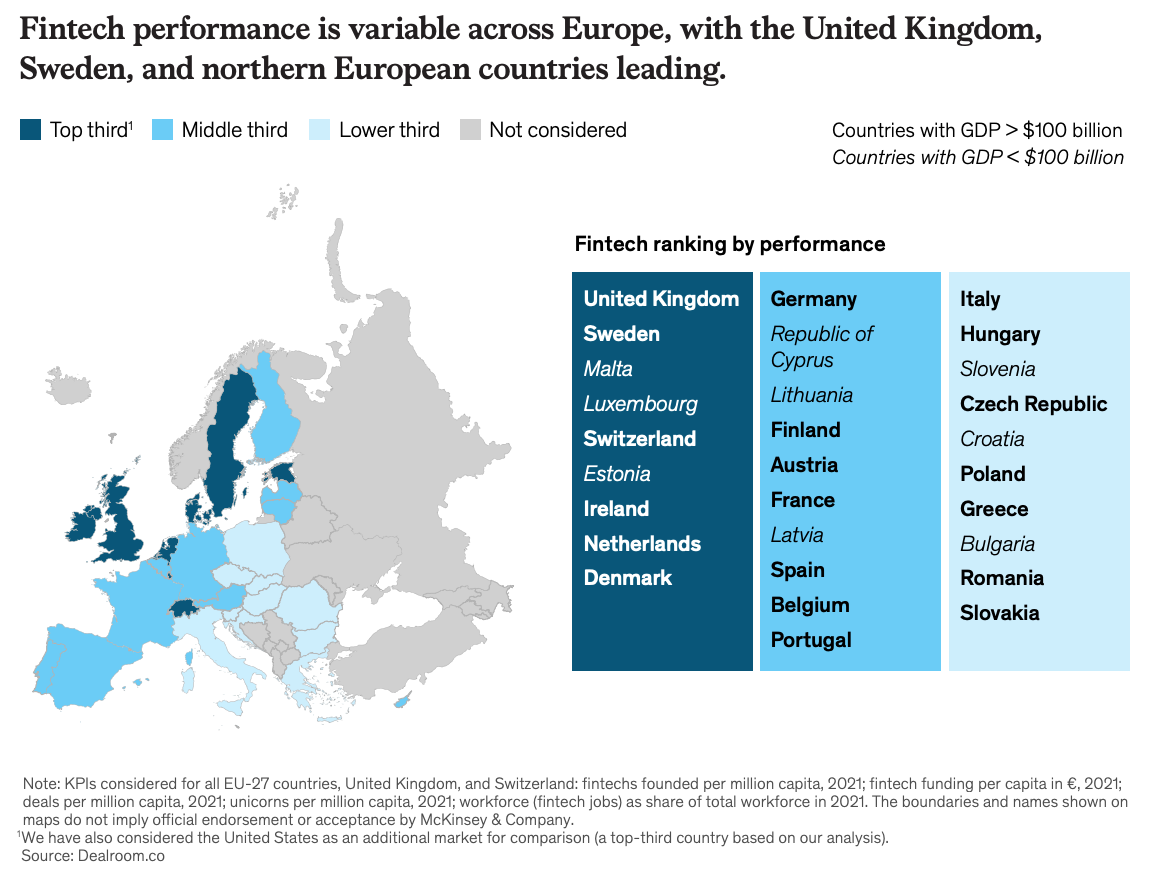

In Europe, fintech activity is growing in virtually all countries, but performance and maturity levels are found to be the greatest in the UK and Sweden, the two countries that are now leading the region for the size of their respective fintech industry, fintech funding, the number of unicorns they house and their fintech workforce, a new analysis by McKinsey found.

Looking at five key performance indicators, namely the number of fintech companies and unicorns each country has, fintech funding activity and deal counts, as well as the size of the fintech workforce, as of 2021, the study found that the UK and Sweden are significantly outperforming their European peers across all these critical performance areas.

They rank at the top of the list, ahead of Malta, Luxembourg and Switzerland, which score high in some areas but fall short in others (workforce for Malta, fintech funding for Luxembourg and unicorn count for Switzerland).

Fintech performance across European countries, Source: Europe’s fintech opportunity, McKinsey, Oct 2022

The UK, Sweden, Malta, Luxembourg and Switzerland are followed by Estonia, Ireland, the Netherlands and Denmark. Together, they make up the top third of the list of countries studied.

Estonia and Ireland perform remarkably well in terms of fintech deal count and the size of their fintech community. They, however, lack fintech unicorns.

The Netherlands, on the other hand, score highly in the number of billion dollar fintech companies it has, as well as in the size of its fintech workforce. But it performs relatively poorly in fintech company founding, as well as in fintech deal count.

Finally, Denmark ranks relatively high in fintech funding and deal activity, but underperforms in the size of its fintech workforce. It also has a relatively low count of fintech unicorns.

These nine countries surpass Germany, Cyprus, Lithuania, Finland, Austria, France, Latvia, Spain, Belgium and Portugal, which make up the second-third of the ranking.

Germany has a relatively large fintech workforce but has a low count of unicorns when taking into account the size of its population.

Cyprus has a vibrant fintech startup scene and a considerable fintech workforce, but underperforms in fintech funding activity.

Lithuania performs well in fintech deal count, but performs moderately in the size of its workforce and fintech funding sum.

Finland and France, meanwhile, score in the average range across all major areas.

The bottom third of the ranking is made up of Italy, Hungary, Slovenia, Czech Republic, Croatia, Poland, Greece, Bulgaria, Romania and Slovakia. Most of these countries have relatively small fintech industries, limited funding activity, and do not have any fintech unicorn.

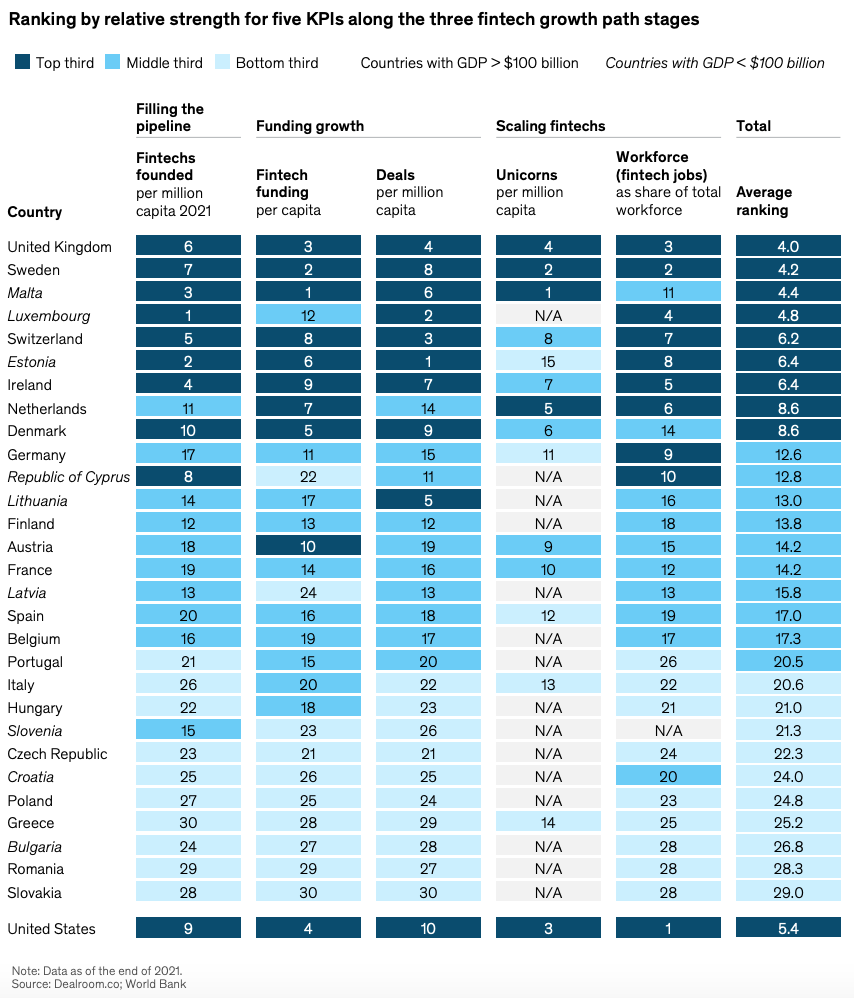

Ranking by relative strength for ve KPIs along the three ntech growth path stages, Source: Europe’s fintech opportunity, McKinsey, Oct 2022

Evidently, findings of the study show a wide divergence of maturity and performance among fintech ecosystems by European country, with substantial gaps between the top one-third and the rest.

If fintech ecosystems in all European countries were able to reach the same level of performance as the best-in-class nations in the region, the upside could be substantial, the report says.

The number of fintech jobs would grow by a factor of 2.7 to more than 364,000; the volume of funding would more than double to almost EUR 150 billion from EUR 63 billion; and valuations would surge by a factor of 2.3 to almost EUR 1 trillion, it says.

But catching up with the leaders will require lower and middle-performing countries to have “a clearly defined programmatic agenda and ongoing commitment,” McKinsey says.

For this, six strategic areas should be focused on. In particular, governments and policymakers should concentrate on simplifying and harmonizing Europe’s fragmented national country regulation, it says. They should also establish a regulatory framework that fosters innovation and provides companies with the necessary conditions to compete domestically and internationally.

Efforts should be made to encourage more diverse and homegrown capital, attract global talent, and support their homegrown fintech companies in expanding overseas.

In Europe, fintech companies have been a force for growth, modernization and customer satisfaction, offering more competitive pricing, easier access, and speedier services.

In each of the seven largest European economies by GDP, namely France, Germany, Italy, the Netherlands, Spain, Switzerland, and the UK, McKinsey claims there is now at least one fintech company among the top five banking services institutions, as measured by market value.

Fintech is also an important source of growth for the overall economy, having created an estimated 134,000 jobs in Europe.

As of June 2022, fintech companies in the region represented a valuation of almost EUR 430 billion, a figure that surpasses the combined market capitalization of the region’s seven largest listed banks.

Europe is also home to some of the world’s most valuable fintech startups. Of the top ten most valuable private fintech companies in the world, three are headquartered in the region, data from CB Insights show: Checkout.com, a UK payment company that’s worth US$40 billion; Revolut, a digital bank based in the UK that’s valued US$33 billion; and Blockchain.com, a software platform for digital assets and cryptocurrency wallet provider based in the UK that’s worth US$14 billion.