In Switzerland, banks and financial institutions have been slow in embracing the open banking movement, a delay that can partly explained by institutions’ conservative corporate culture as well as an overarching fear of losing customers to third parties.

These are some of the findings drawn from a study conducted by the Institute of Financial Services Zug IFZ of the Lucerne School of Business, which sought to understand the banking sector’s views on open banking, determine the roadblocks to adoption, and identify the progress made so far.

The study, which is based on interviews with experts from banks, insurance companies and fintechs and desk research, identified a prevalent belief that opening up channels to fintech startups and other third parties will pose a risk to their business. Almost unanimously, the banks pointed out during the interviews that one of their central strategic goals was to “keep” the customer interface.

Another key roadblock to open banking adoption identified is the fear of change. This resistance often come from employees wanting to protect themselves from the unknown or imagined outcomes of change, as well as from the potential of losing their jobs. Hence, most prefer to stick to the “tried-and-tested” approach, the report says.

In addition to these challenges, the study found that many Swiss banks’ leadership still underestimate the importance of open banking, viewing the trend as a computer science issue rather than a critical strategic priority.

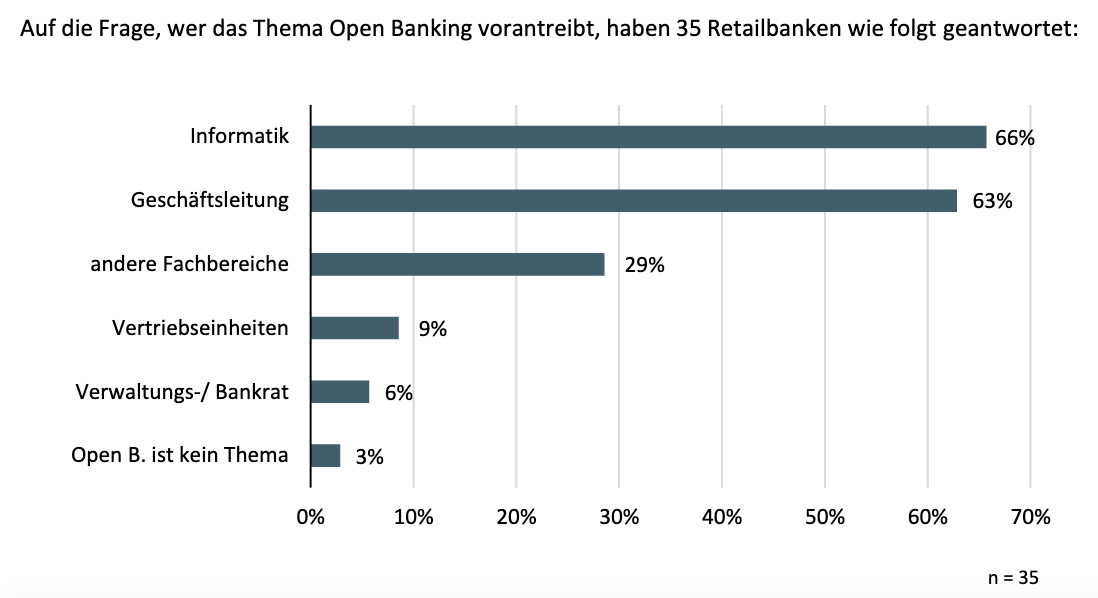

When asked about the driving forces behind their open banking efforts, 66% of 35 retail banks polled indicated their IT department. Management came second at 63%, sales units came fourth at 9%, and the board of directors/council came last at only 6%.

The driving forces behind Swiss bank’s open banking efforts, Source: IFZ Open Banking Studie 2022

Progresses being made

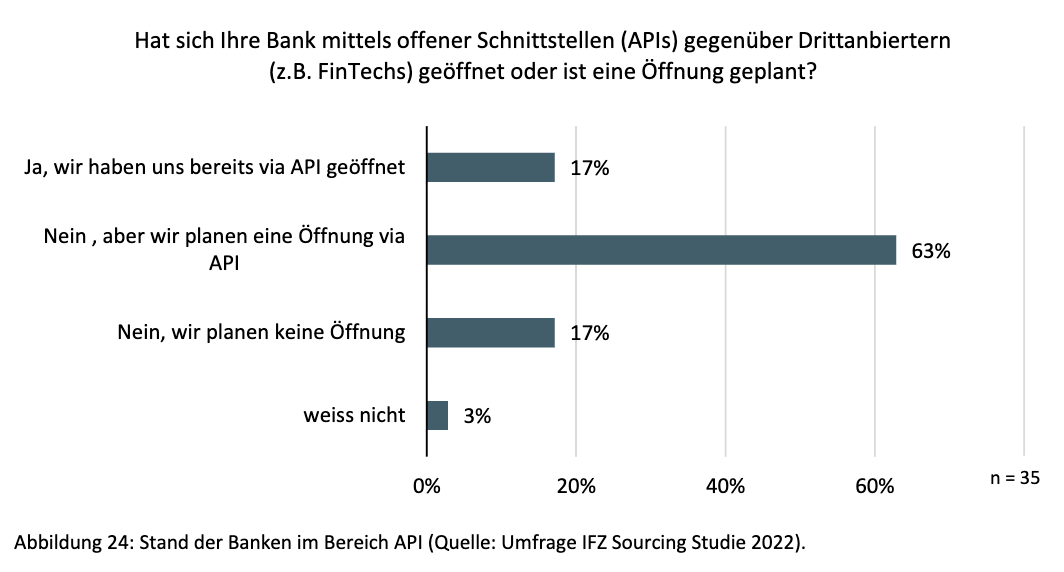

Despite these hurdles, the report notes that progress is being made. The survey of retail banks found that 17% already have open APIs in place. Of those that don’t, 63% shared plans to set up capabilities to connect with third parties.

Has your bank opened up to third-party provider using open interfaces (APIs) or is planning to? Source: IFZ Open Banking Studie 2022

The report notes that discrepancies exist between retail banks, with some, including Valiant, UBS or Hypothekarbank Lenzburg, emerging as early adopters. Others, meanwhile, just started looking into open banking recently.

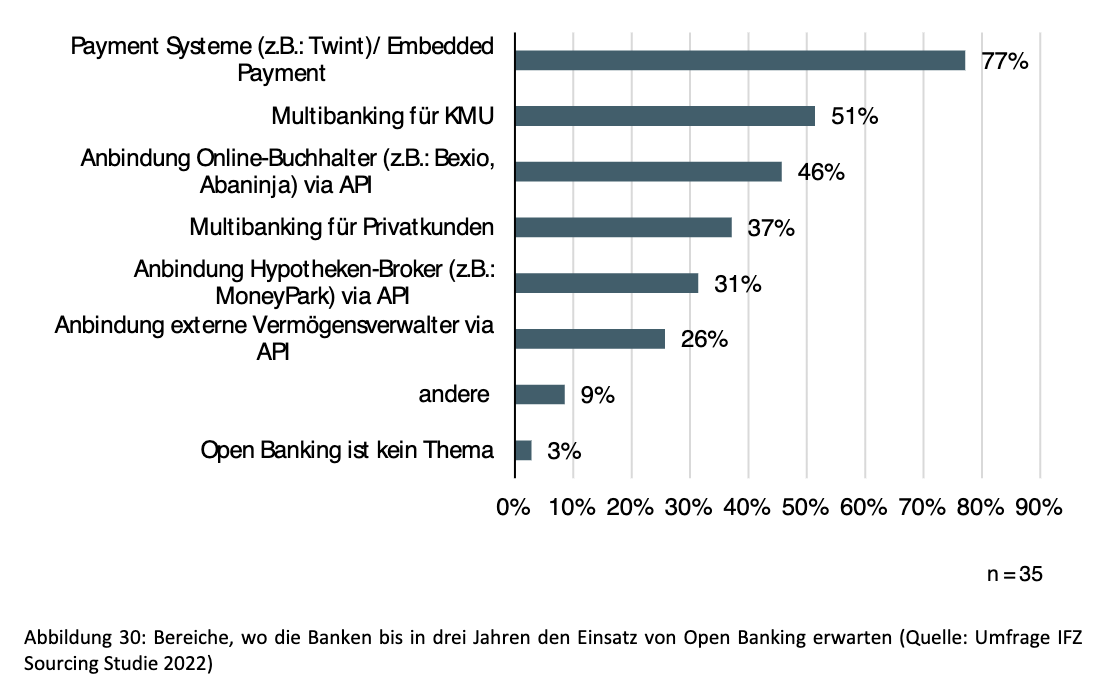

Respondents were also asked in which areas they will be using open banking solutions within the next three years. The results show a broad range of new products and services Swiss retail banks are planning to introduce over the next few years by leveraging the capabilities brought about open banking.

The top five open banking use cases at Swiss retail banks are payments and embedded payments (77%), multibanking services for small and medium-sized enterprises (SMEs) (51%), connection to online accounting software (46%), multibanking services for private customers (37%), connection to online mortgage brokers (31%) and connection to external asset managers (26%).

Areas where banks expect to use open banking in the next three years, Source: IFZ Open Banking Studie 2022

Unlike the European Union (EU) and the UK where open banking is mandated by regulations like PSD2 and the Open Banking Standard, open banking development in Switzerland has been market-driven.

Despite having no formal or compulsory open banking regime in place, the Swiss market has seen promising developments in the field. For example, trade association Swiss Fintech Innovations (SFTI) is working with the industry to develop the so-called Common API Specification for Finance, a set of API standards and specifications for the industry to obey by to enable uniformity and consistency.

Efforts to advance open banking adoption in Switzerland comes at a time when consumers are warming up to the concept.

A 2021 survey conducted by MasterCard found that, although just a few consumers knew what open banking was, consumers showed strong interest in the use cases and opportunities the trend brings.

The research, which polled more than 1,000 consumers from Switzerland in April 2021, found that of those who had not heard of open banking before, 14% showed interest after being provided a generic definition, a level that increased significantly (52%) when consumers were given explanations of real use cases of open banking.

Not only that, but 49% of respondents said that they would be willing to change their primary bank or add a new banking relationship to benefit from at least one open banking-enabled service.

Featured image credit: Edited from Unsplash