How Connected Cars Will Help Drive the Payment Revolution

by Fintechnews Switzerland August 18, 2022Cars are becoming increasingly more connected and are turning into a new mobile source of payment and data.

Juniper Research estimates that by 2026, global transaction volume of in-vehicle payments will exceed 4.7 billion by 2026, up from just 87 million in 2021, an extraordinary growth which will be driven by increasing industry collaboration and initiatives from stakeholders.

According to JP Morgan, connected cars could profoundly transform how people transact, create new business models, and introduce new opportunities for all stakeholders in the industry.

In a new blog post, the bank delves into its key predictions for the future of the connected car market, sharing how it believes car wallets will revolutionize the payment industry, reshape commerce and bring about new shopping experiences.

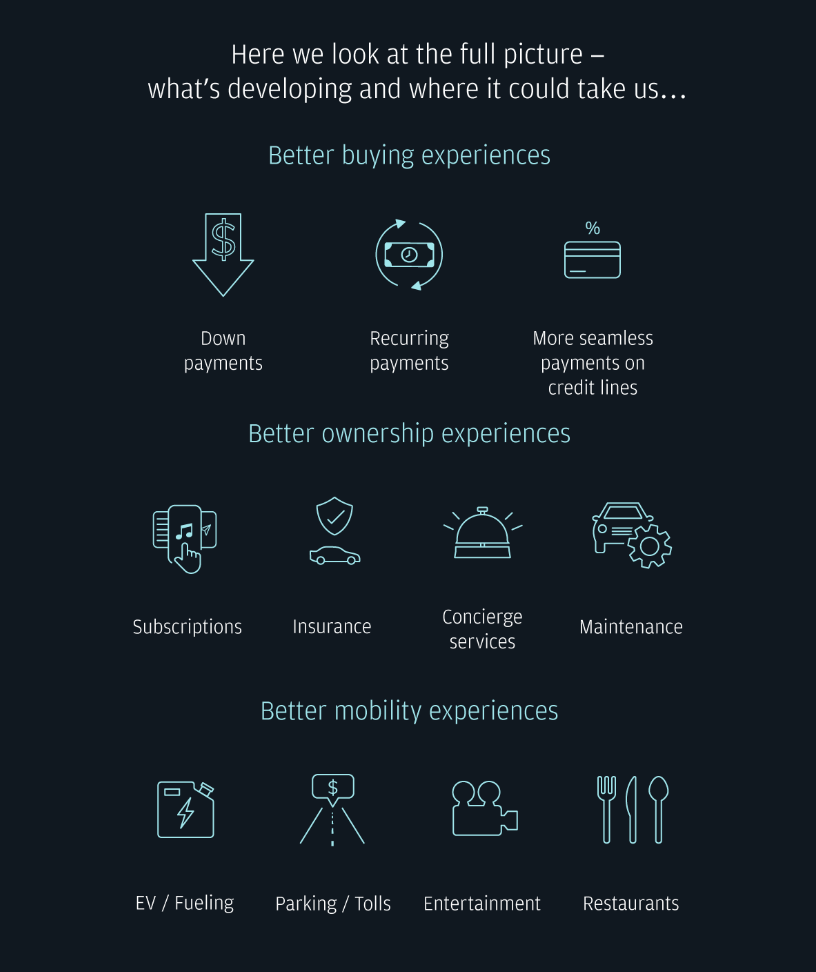

The future of automotive payments solutions, Source: JP Morgan

New shopping experiences

Today’s customers are looking for more convenient digital solutions to spending, a shift that has enticed tech startups, car dealers and banks to develop new shopping experiences and distribution models to cater to consumers’ changing needs.

Carvana, for example, is an online used car retailer that provides a comprehensive online ecosystem for customers to browse for vehicles, get an offer for their trade-in, secure financing and schedule the delivery of their vehicle. The company is fastest growing online used car dealer in the US and was one of the youngest companies to be added to the Fortune 500 List.

Another example cited in the post is WePay, a payments infrastructure provider and Chase company. In the automotive space, WePay facilitates payment transactions, allowing customers to go directly to an auto manufacturer’s website and make a contactless down-payment directly to the dealership. Customers can also request additional products and services like routine vehicle maintenance, parts and accessories right from the auto manufacturer’s website and send payment directly to the dealership.

A wallet on four wheels

In the payment area, connected cars hold promising opportunities both in the business-to-consumer (B2C) and the business-to-business (B2B) fields.

In B2C, a mobile wallet integrated into a connected car can allow drivers to make seamless transactions, whether that’s paying for coffee, parking space or making their car loan monthly payment. A car wallet can also be used by manufacturers and dealerships to allow electrical charging deposits and trade-in credits for use in an ecosystem, creating more value for customers, improving retention and enabling better ownership and mobility experiences.

In B2B, a car wallet can be used by a business to pay for its employees’ travel and expenses, removing the need to report expenses separately and helping mitigating fraud by controlling which types of merchants can receive payments, for example.

A marketplace connecting drivers with merchants and services providers

Like mobile phones became a channel for marketplaces and e-commerce activity, connected cars could potentially take on a similar role, connecting drivers to retailers, gas stations and service providers via their dashboard.

A media company, for example, could use the car as an outlet and offer consumers the opportunity to purchase the goods displayed on the screen via contextual commerce.

Opportunities to develop marketplaces also exist where a customer could potentially be provided with access to a broad range of products and services offered by third parties right from their car. Similar to an app store, the platform would connect third-party suppliers to each other, allow them to collaborate and sell their products and services on the car’s marketplace.

Data monetization

Equipped with sensors, connected cars also offer auto manufacturers with data monetization opportunities, allowing them to gain deeper insights into their customers to provide additional services tailored to their specific needs.

Using real-time data collected from a car, a manufacturer could provide greater insights and advisory services to dealerships and drivers, helping them to curate a personalized user experience that could ultimately lead to greater revenues.

Insurance companies, as well, could use this data to offer pay-as-a-go insurance coverage and personalized pricing options, improve the claims process, and overall deliver a better overall experience.

An enabler for mobility-as-a-service

Finally, JP Morgan believes connected cars have the potential to further fuel the growth of shared mobility, acting as an enabler for new usership and ownership models.

Shared mobility has been a fast-growing industry over the past couple of years, a rise that’s been driven by increased demand for short-term rentals, car sharing options and car subscriptions.

Major auto manufacturers including Toyota, Audi and Jaguar Land Rover all offer options for car subscriptions, while tech-enabled companies like HyreCar and Turo are providing private car owners with the means to rent out their vehicles.

Featured image credit: Edited from Freepik