KPMG Report: Robo Advice Platforms Will Manage US$2.2 trillion Worth of Assets by 2020

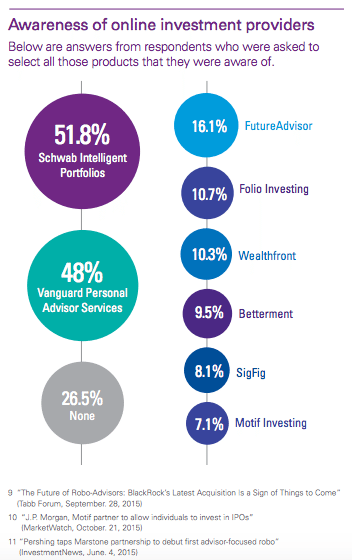

by Fintechnews Switzerland February 24, 2016KPMG surveyed 1,500 bank clients about their awareness of and interest in digital wealth management, or robo-advisors. The firm found that while awareness of the robo advising services of popular fintechs including SigFig, Betterment, Wealthfront and FutureAdvisor (8% to 15%) was relatively low, interest in robo-advisor services was high, with 75% of respondents who said they were “very likely or somewhat likely” to consider robo advising services from their banks.

The factors that contributed to the growth of digital advice, according to KPMG, include the fact that these solutions provide increased transparency, increased accessibility through low or no minimums and fees, enhanced customer experience, as well as their use of exchange-traded funds to build diversified portfolios.

Hence, robo advisors often appeal to less-wealthy investors, given the availability of low-minimum and low-cost portfolios. These solutions also coincide with expanding interest in passive investing.

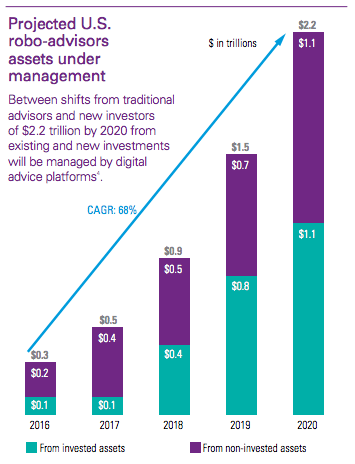

Digital wealth management is changing the investing landscape, the firm said. KPMG estimates that by 2020, robo advisors will be managing US$2.2 trillion in the US.

One population that is particular keen on online wealth management solutions is the millennial generation: 80% of respondents aged between 18 and 34 years old said they would be “very likely or somewhat likely” to consider using robo advisors.

Interesting fact:

“People spanning the financial spectrum are buzzing about “robo advisors,” automated, digital wealth management solutions that have proven attractive to both high net-worth clients and mass market customers. A quick Google search on the term produced more than 683,000 hits and 31,000 news results.”

KPMG advises banks:

“The opportunity for banks is ripe, but you must act now to capture your share of the market. Otherwise your clients will eventually look for these solutions at other institutions.”

Banks should address these points when considering launching a robo advising solution:

Competitive realities: Robo advising might not be right for every traditional bank. How critical is it for a bank to respond to rapidly changing market dynamics? How will the organization differentiate its digital advice offering?

Product options: Digital advice providers generally offer diversified portfolios of low-cost ETFs across multiple asset classes. What product solutions will be offered? What specific bank-brokerage capabilities can a bank leverage to provide compelling and competitive products?

Client opportunities: Existing bank clients are prime targets for robo advising services. What portion of banking clients have investing accounts with an affiliated brokerage?

Cultural capabilities: Banks are expanding investing access to more of their clients and are introducing broader bank-brokerage offerings. Hence, there needs to be increased cooperation and coordination to create a seamless, unified customer experience.

Investing approach: Digital advice is a strong fit for passive investing as executed through a wide range of ETFs. Do internal stakeholders and clients understand the passive investing philosophy and the role ETFs can play? Are they familiar with ETF securities or interested in learning about them? How can a firm’s asset management expertise be leveraged to create competitive and differentiated portfolio offers?

Digital strategy: Access to banking and investing products and services are expanding, and clients are increasingly expecting a unified user experience. What degree of Web and mobile integration currently exists? Do clients have a single sign-on to their accounts via the Web and mobile applications or multiple and distinct platforms?

Partnership opportunities: In many cases, partnerships are be the best approach to debuting robo investing solutions. What potential partners are available to work with?

Read the full report: https://advisory.kpmg.us/content/dam/kpmg-advisory/strategy/pdfs/2016/kpmg-robo-advisors-final.pdf?ct=t

16 Comments so far

Jump into a conversation“robo advisors” I’m curious what it is First time I hear about it.

KPMG estimates that by 2020, robo advisors will be managing US$2.2 trillion in the US.

According to KPMG, robo advisers will manage $2.2 trillion in the United States by 2020.

Enhance your WiFi effortlessly with our expert assistance at wifi wavlink com. Our dedicated support ensures seamless navigation through setup, configuration, and management of your Wavlink network. Connect confidently for an efficient and tailored WiFi experience, optimizing connectivity effortlessly.

Seamlessly access and manage your Linksys Velop network with our expert assistance at the login portal. Our dedicated support ensures a smooth and secure login process, guiding you through configuration and optimization for optimal network performance. Connect confidently for efficient network management.

Streamline your HP wireless printer setup with our expert assistance. Visit 123.hp.com/setup for personalized guidance through a seamless configuration process. Our dedicated support ensures efficient installation, network connection, and software setup, empowering you to start printing with ease.

Streamline your ASUS router setup with our expert assistance. Access the setup wizard on your ASUS router and follow on-screen instructions. Our dedicated support ensures seamless configuration, empowering you to optimize your network settings effortlessly for reliable and efficient connectivity.

Facing issues with your Eufy camera Wi-Fi setup? Our expert team at Assist is here to help. Whether it’s troubleshooting connectivity problems or guiding you through the setup process, we provide reliable support to ensure seamless integration into your home security system.

Indian Servo Controls In is a well-known Manufacturer, Supplier & Exporter of Servo Voltage Stabilizer/Industrial Voltage Regulator, Transformer & Silicon-Power Rectifiers. For More Info, Visit our Website:- https://indianservocontrols.in/

The regulatory landscape is further shaped by judicial interpretations, administrative decisions, and guidance documents issued by the FDA. These documents provide clarity on regulatory expectations, serving as roadmaps for industry compliance and enforcement actions. Moreover, they reflect the dynamic nature of FDA law, evolving in response to scientific advancements, public health crises, and shifting societal norms.

In the quiet moments of early mornings or late nights, the kitchen cabinet becomes a sanctuary for those seeking solace or inspiration. Its doors offer refuge from the chaos of the world outside, inviting introspection and reflection as one arranges jars and cans with a rhythmic precision. Here, amid the clatter of pots and pans, dreams take shape, plans are hatched, and the next culinary masterpiece begins to simmer in the mind.

For Eufy camera reset assistance, locate the reset button on the camera. Press and hold it until the LED indicator blinks. Release the button and wait for the camera to reboot. Once reset, follow setup instructions in the Eufy app. Need further guidance? Contact our support team for prompt assistance.

G-Shock watches are renowned for their robustness and have been on the wrists of adventurers and outdoor enthusiasts for decades. Developed by Casio in the early 1980s, these watches were designed with the intent to create an unbreakable watch. The G-Shock was born out of the determination of an engineer named Kikuo Ibe, who was motivated by a personal incident where a cherished watch broke from a fall. This incident led him to pursue the development of a watch that could resist mechanical shock and vibration.