Spain Business Banking Poised for Digital Transformation

by Fintechnews Switzerland February 2, 2024The Spanish banking sector is poised for significant progress in the area of digital banking, a growth which will be driven by increased innovation in the business banking category, the introduction of the “Ley Crea y Crece” law, and the advent of foreign digital banking leaders in the market, a new analysis by French fintech-focused research reveals.

The report, released on January 09, 2024, explores the growth of the Spanish digital banking scene, delving into the sector’s key players and their growth strategies, and sharing predictions about what lies ahead for the sector.

According to the report, Spain has witnessed considerable growth in digital banking, a sector that currently boasts 28 players encompassing digital outlets launched by incumbent banks, domestic pure-players and global digital banking leaders. These players have captured a remarkable user base exceeding 15 millions by providing intuitive and user-friendly app experiences, streamlined services, and continuous innovation in app functionality.

Looking at the state of digital banking in Spanish, the report says that innovation in Spain has mostly focused on the retail segment, leaving the business segment largely untapped. This year onwards, C-Innovation expects Spanish digital banks to build upon the innovation in retail banking to deepen their penetration in the business banking segment. Harnessing Spain’s embracement of fintech, these players will expand their product offerings and help create a diverse digital banking ecosystem.

The report highlights the introduction of the “Ley Crea y Crece” (Business Creation and Growth Law) as a critical driver of business banking innovation.

“Ley Crea y Crece”, which was approved by the Congress of Deputies in September 2022, is a new regulation designed to facilitate the creation of companies, reduce regulatory obstacles and promote business growth and expansion. Among its key provisions, the law generalizes the use of electronic invoices, establishes measures to combat late payments in commercial operations, and promotes alternative financing by encouraging mechanisms such as crowdfunding, collective investment or venture capital (VC).

The law also removes previous restrictions on the types of banking services non-traditional entities can offer, inviting digital banks to serve the demands of small and medium-sized enterprises (SMEs) and fostering a more competitive banking environment.

These provisions are paving the foundation for neobanks to expand and offer a wider spectrum of services, the report says, delivering promising prospects for expansion and evolution in the years ahead.

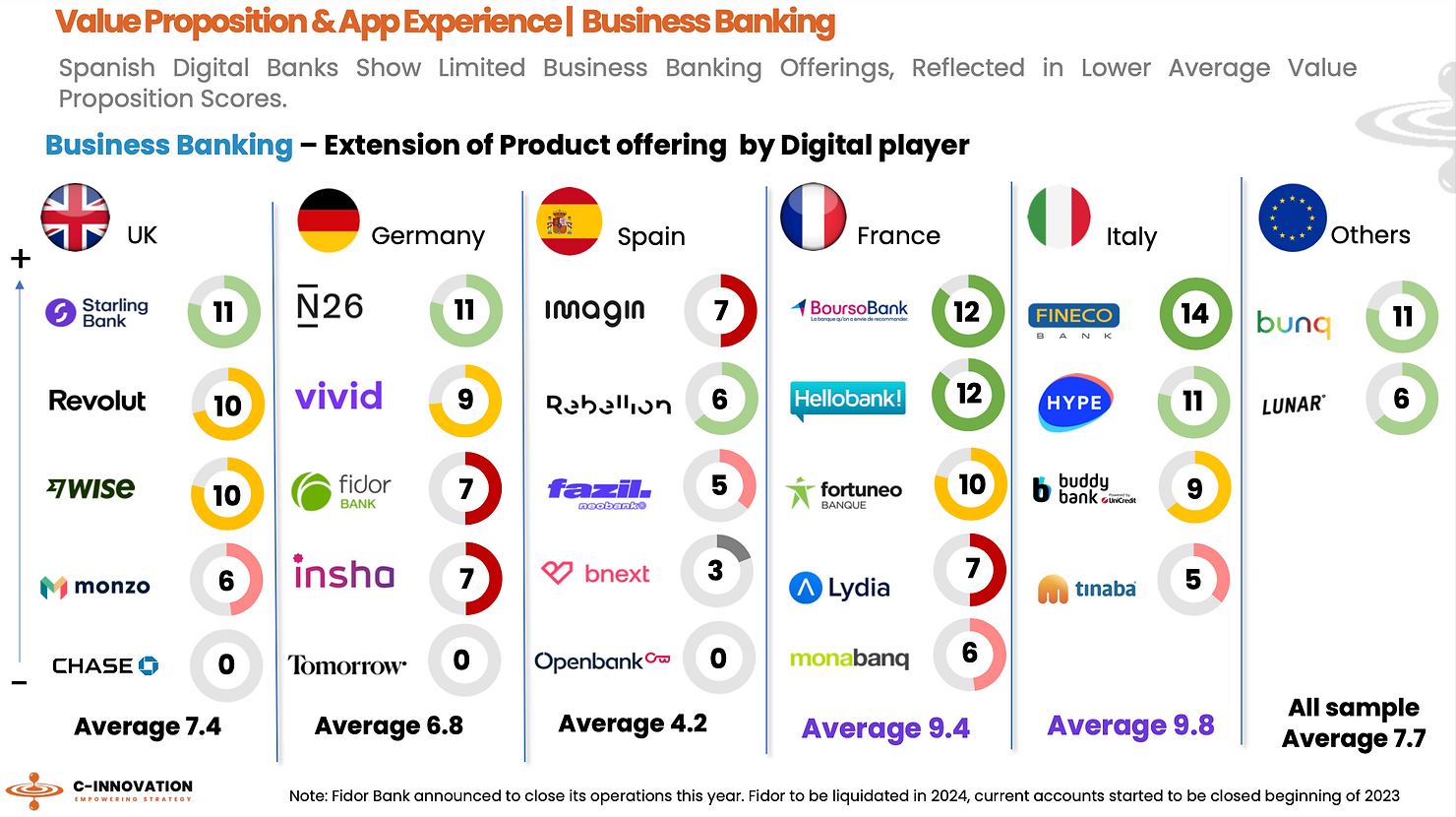

The business digital banking sector in Spain is currently underdeveloped. While domestic digital-only banks including Imagin Bank, Rebellion and bnext, have established a successful presence in retail banking, these players have relatively modest value propositions for their business offerings compared to their European counterparts such as Boursorama and Hello bank!, both from France, Fineco Bank from Italy, as well as Starling Bank from the UK.

The report notes that France’s business finance management provider Qonto has already taken advantage of the new “Ley Crea y Crece” regulation to expand its services to areas once monopolized by incumbents, offering a broader array of services that appeal to SMEs seeking agility, efficiency, and user-focused banking solutions.

Extension of business banking product offering by European digital players, Source: C-Innovation, Jan 2024

Spain’s digital banking landscape

Spain has witnessed rapid growth of its digital banking sector, though this growth has been largely driven by traditional banks. Imagin Bank, a subsidiary of CaixaBank, currently leads the market, providing some 4.2 million customers with a comprehensive digital offering that aligns with the convenience-oriented demands of modern consumers. The figure gives Imagin Bank a 28% market share in Spain.

Imagin Bank operates as a mobile-only bank, offering a banking experience tailored to a younger, tech-savvy demographic. The bank’s services extend beyond traditional banking, integrating lifestyle and e-commerce features such as discounts on entertainment, travel, and technology, to serve as a lifestyle hub.

Standing at the second most-popular digital bank in Spain is Fintonic. The neobanking startup, which focuses on personal finance management, has carved out a niche in the domestic market by offering a centralized platform for users to manage their finances, track spending, and aggregate accounts from different banks. This strategy has allowed it to attract 2.8 million customers in Spain, representing a 19% market share.

At the third position and with 2 million customers is WiZink. Owned by investment firm Varde Partners, WiZink caters to the credit segment of the market, specializing in flexible credit options and competitive savings products. The platform holds a 13% market share.

Openbank, the digital banking arm of the Santander Group, boasts 1.7 million customers, making it the fourth largest digital bank in Spain with a 11% market share. Openbank offers a full range of banking services from standard checking and savings accounts to investment and lending products.

In addition to homegrown brands and players, Spain is also witnessing the advent of global digital banking leaders. Names such as Revolut from the UK and N26 from Germany are gaining traction in the country, now boasting a combined 3 million customers, which represents a remarkable 20% market share.

These companies have been aggressively expanding their footprint in Spanish market, the report says, focusing on developing appealing suites of services encompassing products such as remunerated accounts, small consumer loans, and the integration of popular domestic payment methods such as Bizum.

Spain’s digital-only banks, Source: C-Innovation, Jan 2024

Featured image credit: Edited from freepik