After experiencing record investment volumes in 2021, venture funding is dropping significantly this year amid hiking inflation rates, political instability and tanking stock prices. Investors are scaling back their investment pace significantly, and though many startups are still holding strong and enduring the chaos, dozens have shut down.

Since the beginning of the year, at least 11 fintech companies have closed down, according to CB Insights. A majority of these startups folded due to their inability to raise fresh capital, as was the case for proptech startup Reali and neobank Bank North, while others, like Neufund and LendUp, crumbled in the face of regulatory pressure and legal issues.

Of the 11 fintech startup failures reported, four of them – CommonBond, Reali, Volt Bank and LendUp – were rather large and costly ones, involving startups that had raised US$100 million and up, the data show.

Student loan lending startup CommonBond, which had secured a total of US$1.3 billion in disclosed funding, said in September that it will be “winding down” its operations after its core businesses took a major big during COVID-19.

Reali, a real estate and fintech platform that had raised US$292 million in funding, announced in August that it will begin a shutdown and will be laying off most of the workforce on September 9, citing “challenging real estate and financial market conditions.”

In Australia, Volt Bank, the first exclusively online bank to secure a banking license in the country, said in June that it would shut down, returning deposits and selling its mortgage book after failing to raise sufficient funds to support the business. The digital bank had raised US$102 million.

Finally, LendUp, a payday lending company, was forced by the US Consumer Financial Protection Bureau to cease making new loans and collecting some outstanding loans in December 2021 for “repeatedly lying and illegally cheating its customers,” the regulator said. LendUp had secured US$366 million.

Other significant fintech failures this year include Bank North, a challenger bank that raised US$96 million before running out of cash and collapsing in October; Propzy, a Vietnamese real estate technology platform that had raised US$33 million but ceased operation suddenly in September, citing the impact of the pandemic and unstable global financial situation due to the Russia-Ukraine conflict; B3i Services, an insurance blockchain consortium that had secured US$26 million but which filed for insolvency in July following unsuccessful funding rounds; and Neufund, a security token platform that closed down in January after raising a total of US$19 million.

The other three fintech startups that went belly up this year and which are highlighted in the CB Insights report are Wingocard, a teen financial literacy app that shut down in May; AskRobin, a credit marketplace for unbanked populations went out of business in January after reaching nearly two million customers; and Binance Asia Services, the Singapore arm of cryptocurrency exchange Binance that withdrew from the city-state and closed in February.

2022 has been a trying year for the global fintech scene amid plunging funding activity and a turbulent economy that have forced players to make serious job cuts.

Klarna, a buy now, pay later (BNPL) leader, reduced its headcounts by about 10% in May, citing pressure from investors to slim down its operations. Klarna lost more than US$580 million in the first six months of 2022.

Brex, a corporate spend management once valued US$12.3 billion, laid off 11% of its staff this year as part of a restructuring.

German digital bank N26 reported in October a wider loss for 2021 and a slowing in customer growth. N26’s 2021 loss increased to EUR 172 million from EUR 151 million in 2020. The bank added one million new customers last year, down from the two million customers that were added in 2020.

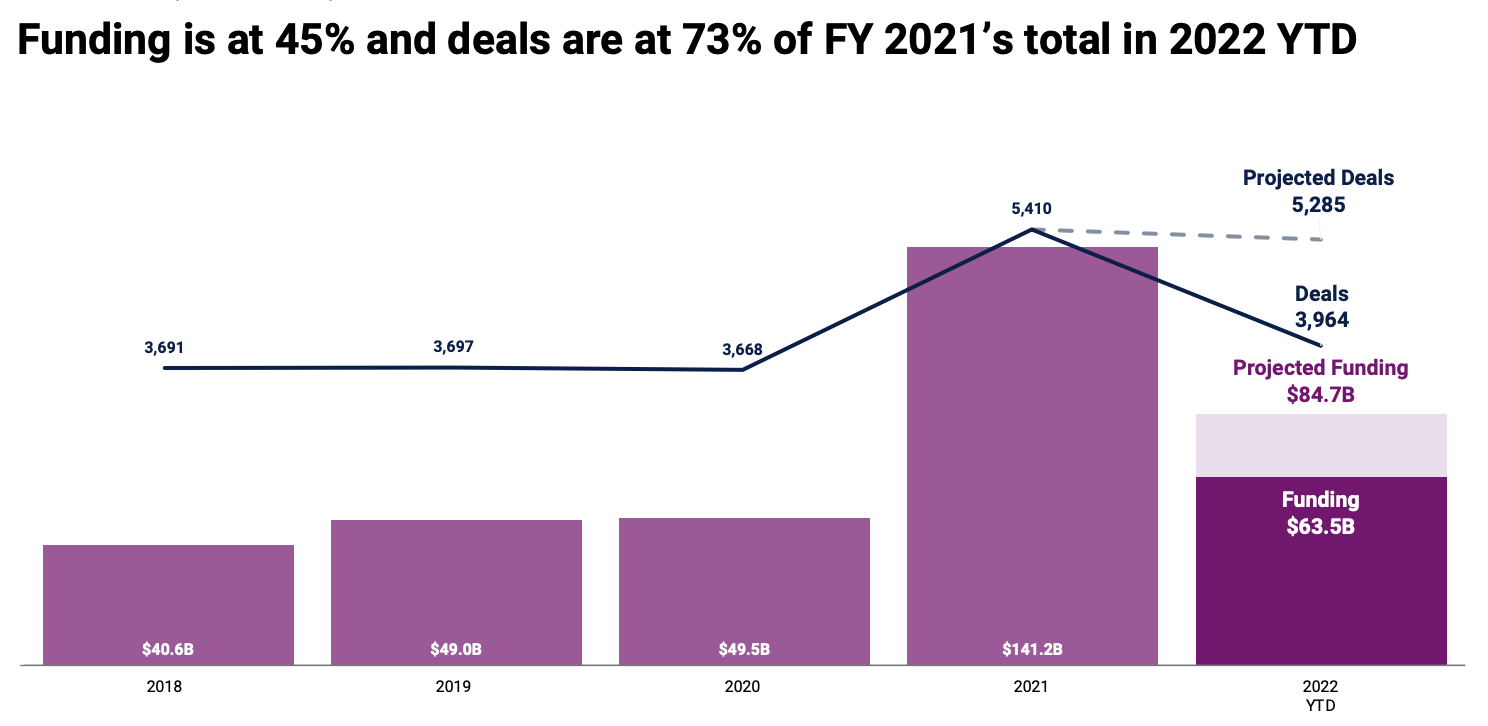

Global fintech funding this year reached US$63.5 billion in Q3 2022, a sum that represents just 45% of 2021’s total of US$141.2 billion, data from CB Insights show.

Global fintech funding, Source: State of Fintech Q3 2022, CB Insights, Oct 2022

Featured image credit: Edited from Freepik