Payment Incumbents Ramp up B2B Payment Innovation Efforts

by Fintechnews Switzerland September 27, 2023Innovation in consumer payments has progressed tremendously over the past years, pushed by demand for more efficient and secure methods of paying for goods and services both online and cashlessly.

But while digitalization has flourished in the consumer payment area, innovation in business-to-business (B2B) payments has somewhat lagged behind, felling to witness the same momentum.

Aiming to tap into opportunity and get a bigger share of the US$125 trillion global B2B payment market, some of the world’s largest payment firms are ramping up efforts to deliver new and innovative products for faster, more efficient and more secure business transactions.

Visa pushes for B2B payment network expansion

Visa has announced a series of partnerships over the past year focusing on enhancing its B2B payment offering and expanding the reach of its B2B payment network. Just this month, the company unveiled a partnership with Swift to improve connectivity between their respective networks and provide financial institutions on both networks with more routing options for their business customers as well as real-time status and updates.

As part of the collaboration, payments going through Visa B2B Connect, the company’s payment network for bank-to-bank cross-border business transactions, will be able to have upfront checks using Swift Payment Pre-Validation. Additionally, the two networks will work together to increase end-to-end transaction visibility by using high-speed Swift GPI capabilities and tracking data.

Swift GPI, which stands for global payment innovation, is a service offered by Swift to make international payments faster and to be able to track their status in real time, from the moment the funds are sent to when they arrive. The service also allows users to get a breakdown of the fees that are collected by the intermediary banks.

Swift GPI was launched in 2017 and has since been adopted by more than 4,200 banks and 60 market infrastructures.

Besides its partnership and integration with Swift GPI, Visa is actively working on expanding its Visa B2B Connect network, adding the likes of CB International Bank, a US-based commercial bank, Freedom Finance Bank Kazakhstan, Krungthai Bank from Thailand, Bank Muamalat from Malaysia, and German software company SAP into its list of partners.

Launched in 2019, Visa B2B Connect is a platform developed by Visa to facilitate cross-border B2B payments. It leverages innovative technologies, including elements of blockchain, to simplify the traditionally complex and time-consuming process of international B2B transactions, and aims to provide businesses with a fast, secure, and transparent way to process corporate cross-border payments.

Visa CEO Ryan McInerney said on the company’s Q2 2023 earnings call that roughly 30 banks across 20 countries have so far signed to Visa B2B Connect, with payments routed to 90 countries globally.

Mastercard expands its B2B payment offering

Mastercard, meanwhile, has been focusing on enhancing its business payment offering. Last year, it launched Instant Pay, a virtual card solution for instant B2B payments integrated with its B2B payment product, the Mastercard Track Business Payment Service. In 2023, the firm introduced Mastercard Receivables Manager, a new solution that streamlines the way businesses accept and process virtual card payments, and which helps them with invoice reconciliation.

Mastercard has also onboarded a number of customers to its commercial network over the past year, including Canadian financial services provider BMO, American paytech company Priority Technology and payment specialist Transcard.

Mastercard’s key B2B payment proposition is the Mastercard Track Business Payment Service, a global open-loop commercial network that’s designed to simplify and automate the exchange of payment information between suppliers and buyers. The service is a specific component of the broader Mastercard Track global trade platform which the firm launched in 2018 to simplify the complex and fragmented global trade ecosystem by providing a centralized framework for business interactions.

AmEx pursues business payment network ambition

American Express (AmEx) is the latest major card payment network to be developing its own B2B payment network. The company is building up a suite of B2B capabilities for both buyers and suppliers through new product development, mergers and acquisitions (M&A) deals, and partnerships.

Most recently, it announced plans to acquire Israeli B2B payment automation company Nipendo. Nipendo’s platform allows businesses to easily connect, communicate, and automate procure-to-pay processes, including accounts payable and receivable, and works alongside a company’s existing systems. AmEx intends to integrate Nipendo’s team, technology, and capabilities to expand its differentiated offerings for businesses.

The deal followed the launch of Amex Business Link in December 2022, a B2B solution for American Express’ network participants; partnerships with accounts receivable players BillTrust and Versapay; as well as the acquisition of Acompay, a digital payment automation solution for accounts payable departments, in 2019.

The rise of digital payments

The B2B payments landscape has been undergoing significant changes, driven by technological advancements, evolving business needs, and regulatory shifts. Payment methods are evolving and while traditional methods such as cash, checks and wire transfers, still hold a significant share in many regions, digital methods are gaining traction.

Mastercard reported observing a shift to digital B2B payments since COVID-19 and said that small businesses are increasingly adopting digital tools to modernize business payments, including payment collection and electronic invoicing.

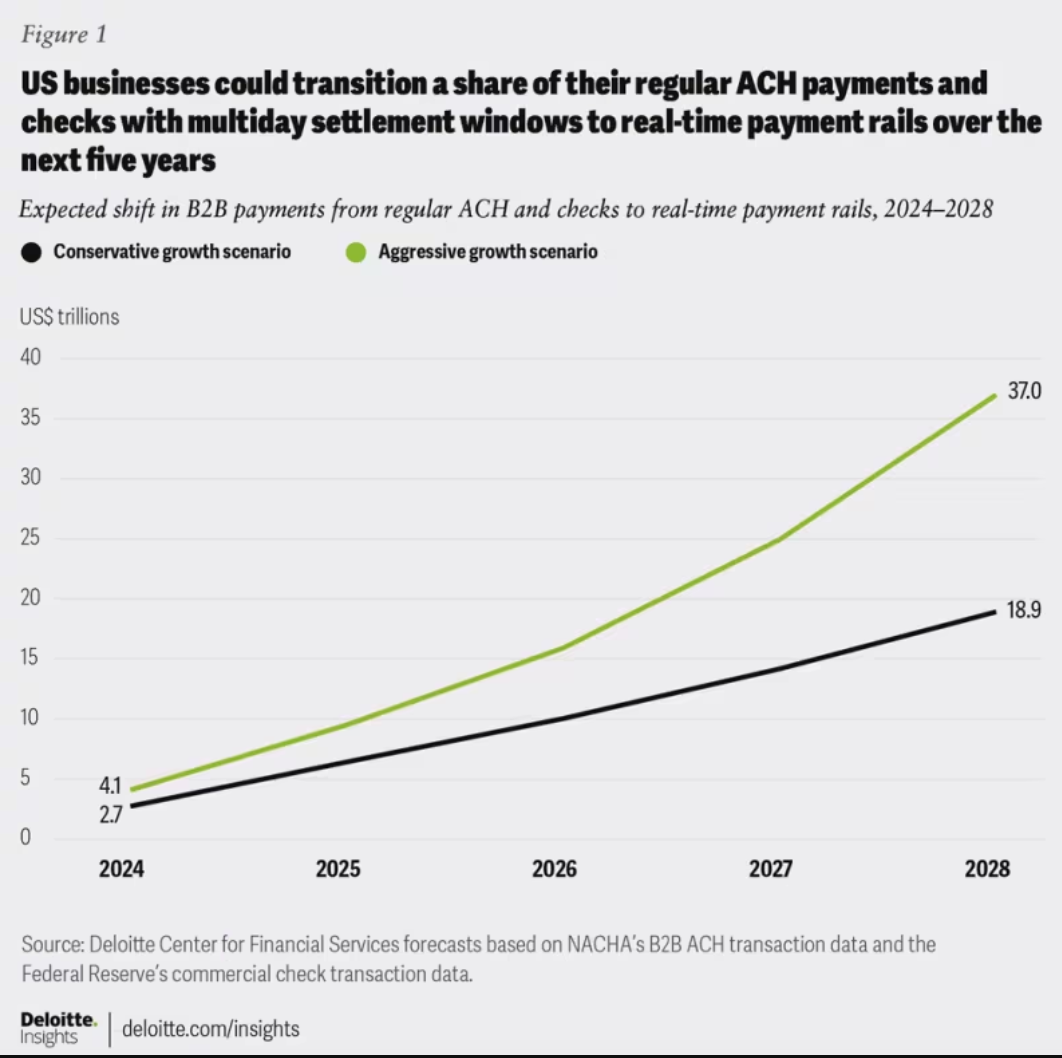

Real-time payments, which run on dedicated networks that enable electronic payments to be processed in real time, 24 hours a day, 365 days a year, are projected to divert as much as US$37.0 trillion in B2B payments away from checks and regular automated clearing house (ACH) payments in the US by 2028, consulting firm Deloitte estimates.

Expected shift in B2B payments from ACH and checks to real-time payment rails, 2024-2028, Source: Deloitte, Jul 2023

Featured image credit: Edited from freepik