EU Parliament Economic and Monetary Policies Unit Cautions ECB on Digital Currency Launch

by Fintechnews Switzerland May 9, 2023The European Central Bank (ECB) is considering launching a retail central bank digital currency (CBDC), seeking improved payment efficiency, innovation and monetary sovereignty. However, there are several concerns about whether a so-called digital euro would be a good idea.

Against this backdrop, the central bank should refrain from issuing a CBDC hastily, and should wait until new favorable elements in favor of the initiative emerge, a new paper by the Economic Governance and EMU Scrutiny Unit, a department within the European Parliament responsible for monitoring and analyzing economic and monetary policies, says.

The document, prepared at the request of the European Parliament’s Committee on Economic and Monetary Affairs (ECON), argues that the risks and imponderables of a CBDC appear to be stronger than the arguments in favor of a digital euro.

One concern outlined in the paper is that a CBDC may change the relationship between the central bank and commercial banks, and that outcomes are impossible to predict.

The ECB has said that in the event of a retail CBDC being launched, front-end functions of the payment and deposit ecosystem would be outsourced to private institutions, including banks and payment services providers. These intermediaries would be in direct contact with end-users, while the ECB would manage centralized accounts and cooperate with commercial banks in the settlement function.

This setup implies that commercial banks would offer services to the central bank, while also competing for the collection of deposit funds. This new relationship would alter the incentive structure in a way that’s impossible to assess at the time being, the report says.

Another concern outlined in the paper relates to the risk of financial instability created by safe accounts that are fully government-backed.

Compared with commercial banks deposits which are prone to the risk of loss, ECB deposits are risk-free because the central bank can always print money to reimburse its debts.

In a banking crisis, depositors become aware of this risk and tend to move away from risky deposits. Since a digital euro would offer a risk-free alternative to bank deposits, a CBDC may accelerate the mobility of deposits and hence, the risk of disruptive bank runs. This may cause damaging outflow of liquidity, the report says.

The paper notes that the digital euro project is part of a global trend towards the introduction of CBDCs, with many central banks exploring the concept at different stage. Against this backdrop, liaison and coordination among central banks are recommended to avoid distortions and adverse effects on any parties.

The digital euro

The ECB is currently working with the national central banks of the euro area to investigate whether to introduce a digital euro. The idea would be to develop an electronic equivalent to cash that would complement banknotes and coins which would provide consumers with an additional choice about how to pay.

The authority published the third progress report on the project in April, presenting a set of design and distribution options for the retail CBDC.

In particular, the ECB proposes for the digital euro to be only accessible to euro area residents, merchants and governments in its initial releases. In further releases, consumers from selected third countries may also gain access to the CBDC. The report also anticipates the potential provision of cross-currency functionalities with other CBDCs outside the euro area by establishing interoperability between the digital euro and other equivalent systems.

The digital currency would be distributed by payment services providers and made available via existing banking apps or via an app provided by the Eurosystem, the monetary authority of the eurozone, the report says. Supervised intermediaries distributing the digital euro would be required to provide a set of mandatory core services to end-users and could offer additional services.

The ECB commissioned last year a study to understand people’s views on specific features of a potential digital wallet. The study, which polled consumers and industry stakeholders in all euro area countries from December 2022 to January 2023, found that person-to-person money transfers and offline payments were considered among the most useful features for Europeans. Participants also shared interest in budget management tools and conditional payments, including payment on delivery and pay-per-use.

The European Commission is set to propose a regulation establishing a digital euro in the second quarter of 2023. By the second half of the year, the Eurosystem is expected to present a high-level comprehensive design for the digital euro, comprising all the design choices and elements described by the three previous progress reports produced by the ECB.

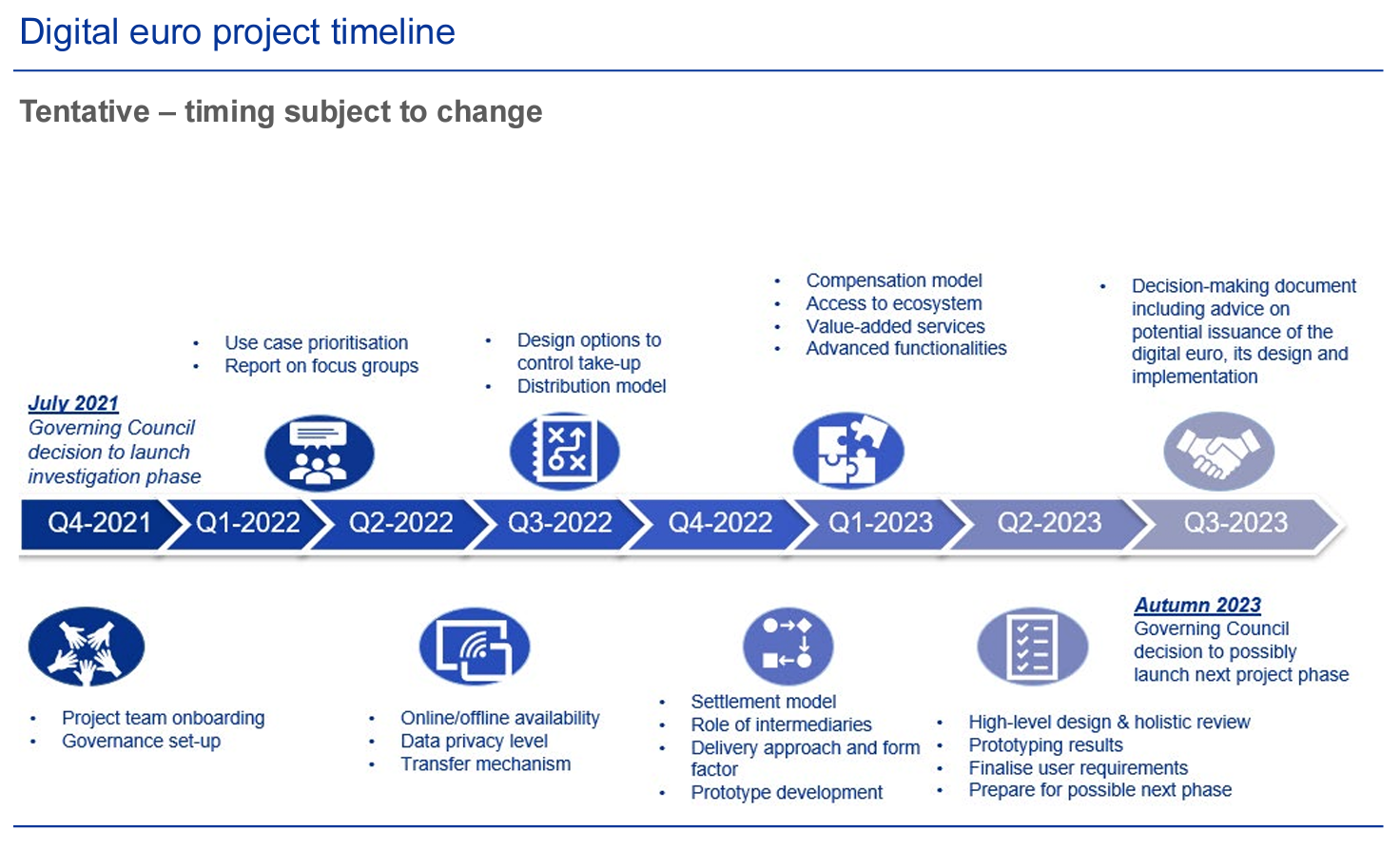

Digital euro project tentative timeline, Source: European Central Bank, April 2023

Featured image credit: Edited from Freepik