QR Code and Instant Payments are Fueling the Growth of Non-Cash Transactions

by Fintechnews Switzerland October 25, 2022The pandemic prompted businesses and customers to embrace digital technologies and non-cash payment methods, fueling the adoption of innovative payment methods like QR code payments, digital wallets, and account-to-account (A2A) payments.

Adoption of digital payments among consumers and businesses will continue to rise in the years to come, driven by growing infrastructure improvements, market maturity and demand from customers for convenient, tech-enabled solutions, a new report by French information technology and consulting firm Capgemini says.

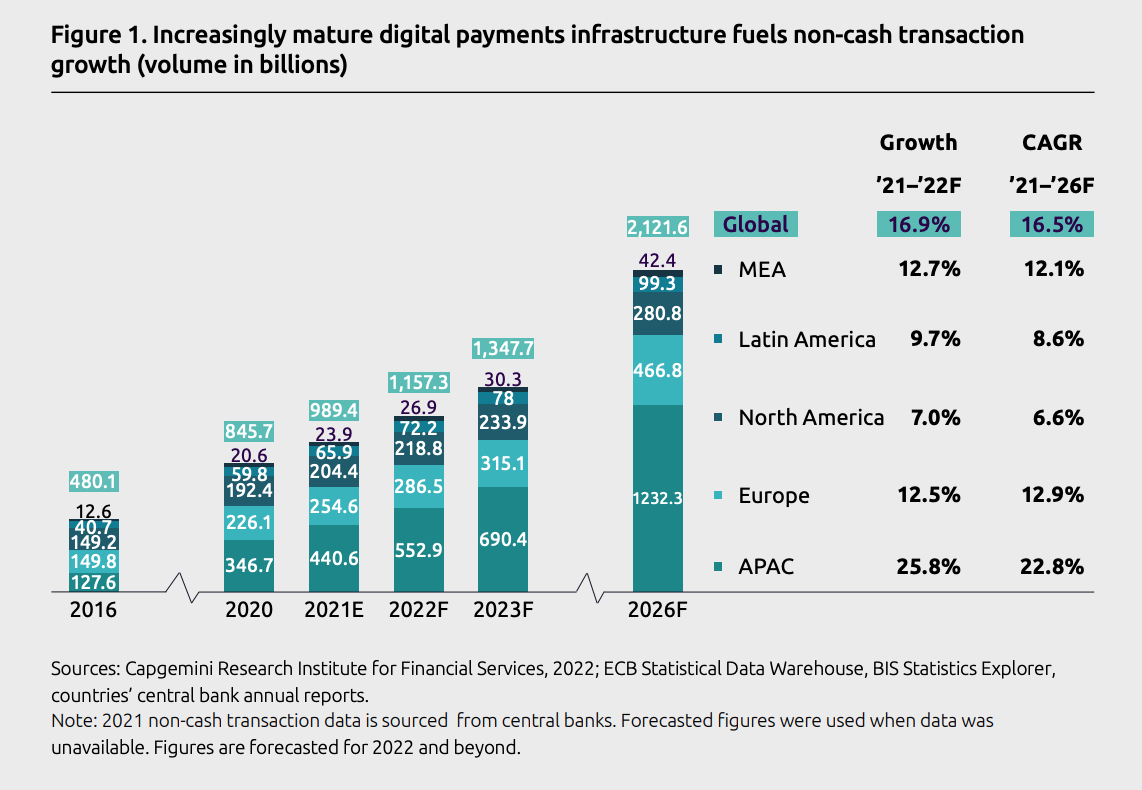

Between 2021 and 2026, non-cash transactions are projected to record a 16.5% compound annual growth (CAGR), rising from 989.4 billion transactions in 2021 to more than 2.1 trillion in 2026.

Increasingly mature digital payments infrastructure fuels non-cash transaction growth (volume in billions), Source: World Payments Report 2022, Capgemini

During that period, new payment methods, like instant payments, e-money, mobile and digital wallets, A2A and QR code, will rise in prominence, with their share growing from 17% of overall non-cash transaction volume in 2021, to 28% in 2026.

Estimates from Capgemini corroborate with projections made by other firms which forecast strong growth in usage of innovative payment methods in the years to come.

Independent research firm Juniper Research forecasts that global QR code payment users could reach 2.2 billion by 2025, up from 1.5 billion in 2020. This implies that almost 29% of all mobile phone users worldwide would be using QR code payments by then.

Similarly, instant payments are on track to a CAGR of around 29% between 2021 and 2025, reaching 428 billion in volume.

Meanwhile, A2A payments are expanding rapidly, especially in emerging markets, according to a new report by the Boston Consulting Group (BCG). In Brazil, PIX reached 122 million registered accounts in less than two years in operation. The number represents over half the country’s population. And in India, Unified Payments Interface (UPI), which was launched in 2016, was handling transaction volumes roughly 11 times those of credit and debit cards combined by 2021.

Moving forward, the growth of A2A real-time payments will only accelerate, thanks to continued investments in infrastructure modernization, BCG says, citing ongoing initiatives such as the RTP system in the US, which is scheduled for launch in 2023 and P27, a pan-regional payments system involving the Nordic countries.

Finally, e-money transactions are expected to witness a similar growth rate of about 27% between 2021 and 2026, to reach about 161 billion in volume. This growth will be driven by increased adoption of digital wallets, which Juniper Research forecasts will see 4.4 billion unique users by 2025.

New payment players gain attraction among SMEs

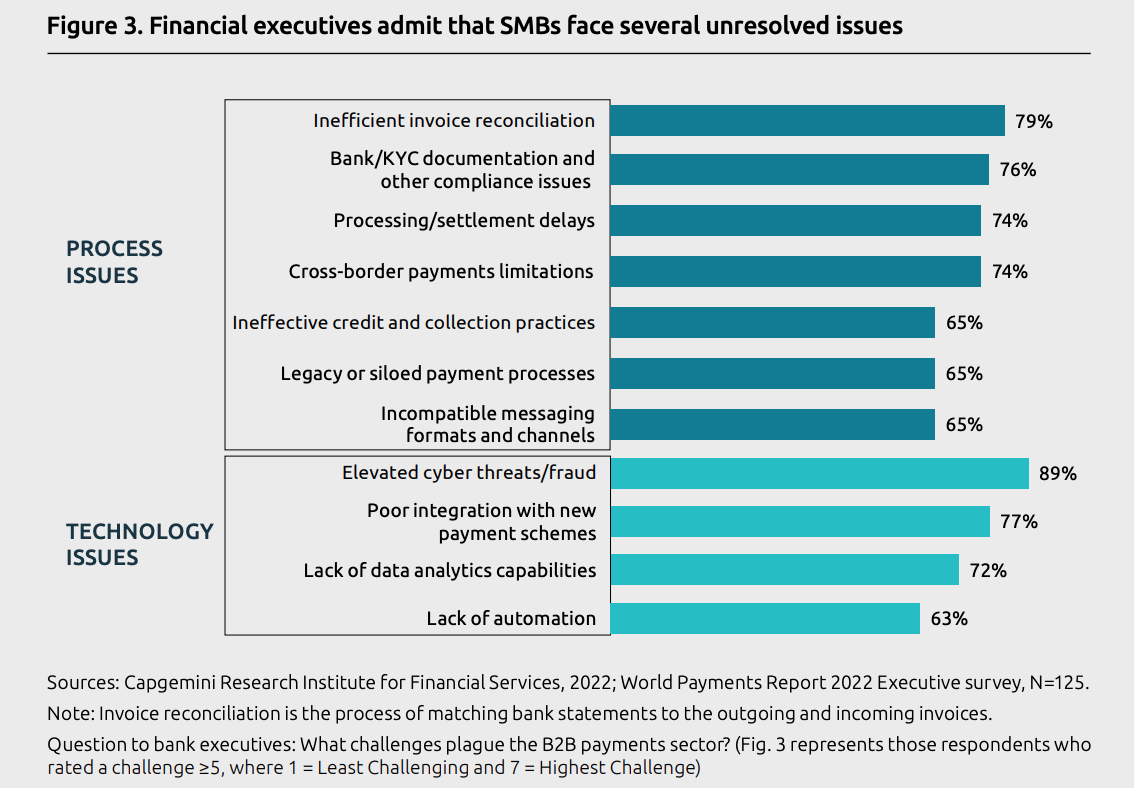

Changing consumer preferences and demand for streamlined customer journeys have pushed merchants to turn to digital solutions, the Capgemini report says. But a survey of 150 small and medium-sized enterprises (SMEs) as part of the study found that traditional banks and payment service providers are missing the mark when it comes to meeting SMEs’ needs.

Financial executives admit that SMBs face several unresolved issues, Source: World Payments Report 2022, Capgemini

Of the SME leaders surveyed, only 11% of respondents said they were happy with their banking relationships, 44% said they were dissatisfied, and 45% were indifferent. The result is that 89% of SMEs indicated being reconsidering relationships with their primary banks across various product categories.

But digitalization has opened the door to new-age players that are actively introducing innovative value propositions across the business-to-business (B2B) payments value chain.

Banking Circle and Currency Cloud, for example, provide global virtual payments and account networks. TransferMate is a paytech company that aims for end-user cross-border payments propositions. And Wise, formerly known as TransferWise, offers global multi-currency wallets to SMEs that reduce transfer costs while offering a higher level automation.

At the same time, several mature fintech companies are stepping up their B2B engagement. Players like Stripe, PayPal, Starling, Revolut, Block (formerly Square), and Wise are developing full-fledged digital ecosystems that bundle core payment services with other financial products like insurance policies, near-banking products like capital management and advisory, and non-financial products such as legal services and human resources, to offer a convenient one-stop value proposition for SMEs.

Ecosystems and marketplaces are an attractive strategy for new-age paytech companies, the report says. Ecosystems increase client intimacy and stickiness. They also expands client engagement touchpoints, providing players with richer and more diverse customer data which can then be used to further personalize services and boost long-term loyalty and retention. Finally, ecosystems can also help to harness untapped revenue streams.

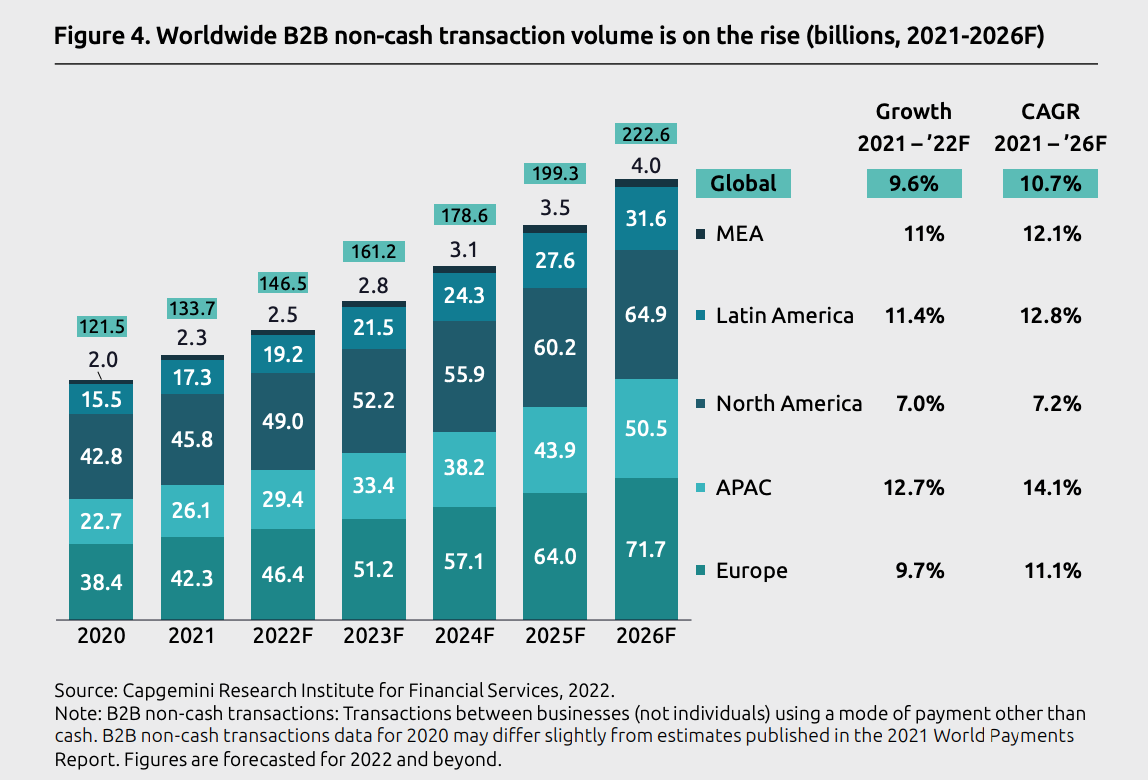

Like retail digital payments, B2B digital payments have experienced steady growth over the past years. Adoption will continue rising in the coming years, with worldwide B2B non-cash transaction volume forecasted to grow 10.7% per year between 2021 and 2026 to reach 222 billion, according to Capgemini.

Worldwide B2B non-cash transaction volume is on the rise (billions, 2021-2026F), Source: World Payments Report 2022, Capgemini

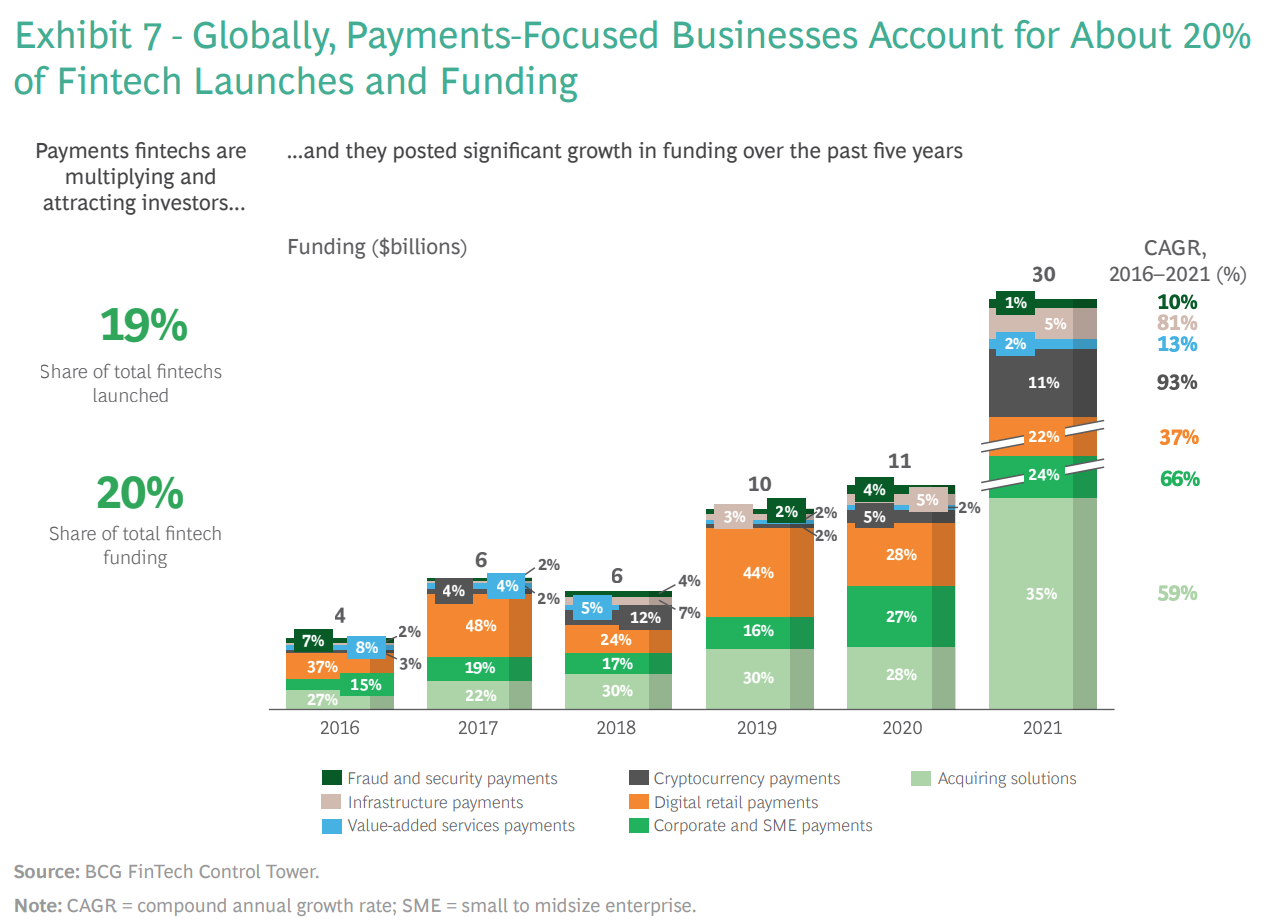

Over the past years, paytech has been one of investors’ favorite fintech segments. Between 2016 and 2021, paytech companies accounted for roughly 20% of cumulative fintech equity funding raised during the period, according to BCG.

In H1 2022, investors funneled US$11 billion into payment-related fintech companies, lower than 2021 funding levels, but still well above the amounts generated in 2019 and 2020.

Payment fintech funding between 2016 and 2021, Source: Global Payments Report 2022, Boston Consulting Group